200% Return in 1 Day

A Case Study and a Pitch

You must have read the title and thought, “Ha, this can’t be right.” I understand. I wouldn’t have thought it was possible before experiencing it 2x in the last 2 months.

Before getting into it, let me stop and say 1) I attribute a lot of these outcomes to luck, 2) Shout out to Michael Liu from Capuchin Capital for coaching me on this strategy (check him out if you don’t know him), and 3) And the tiny bit that is left, I attribute it to the willingness to remove preconceived ideas from my mental biases.

The Case Study - SNSE 0.00%↑

Sensei’s story centered on SNS-101 (solnerstotug), a drug candidate targeting the VISTA checkpoint pathway, one of the more challenging areas in immuno-oncology. The science behind it was compelling. Many VISTA-directed therapies tend to bind too heavily to healthy immune cells in the bloodstream, which can limit their effectiveness and raise the risk of toxicity. Sensei’s solution was to design an antibody that would be more selective in the acidic tumor microenvironment.

The inflection point came in October 2025. After sharing Phase 1 data, management concluded that the results were not strong enough to support continued development. On October 30, 2025, the company formally discontinued SNS-101 and launched a strategic review. That moment is central to the case, because it marked Sensei’s transition from an operating biotech focused on drug development to a company exploring financial or strategic alternatives.

By February 2026, the situation became even more compelling. Sensei expanded its board and added Phillip Donenberg, a director with a track record in biotech restructurings and reverse mergers. That was the point when the story really caught my attention.

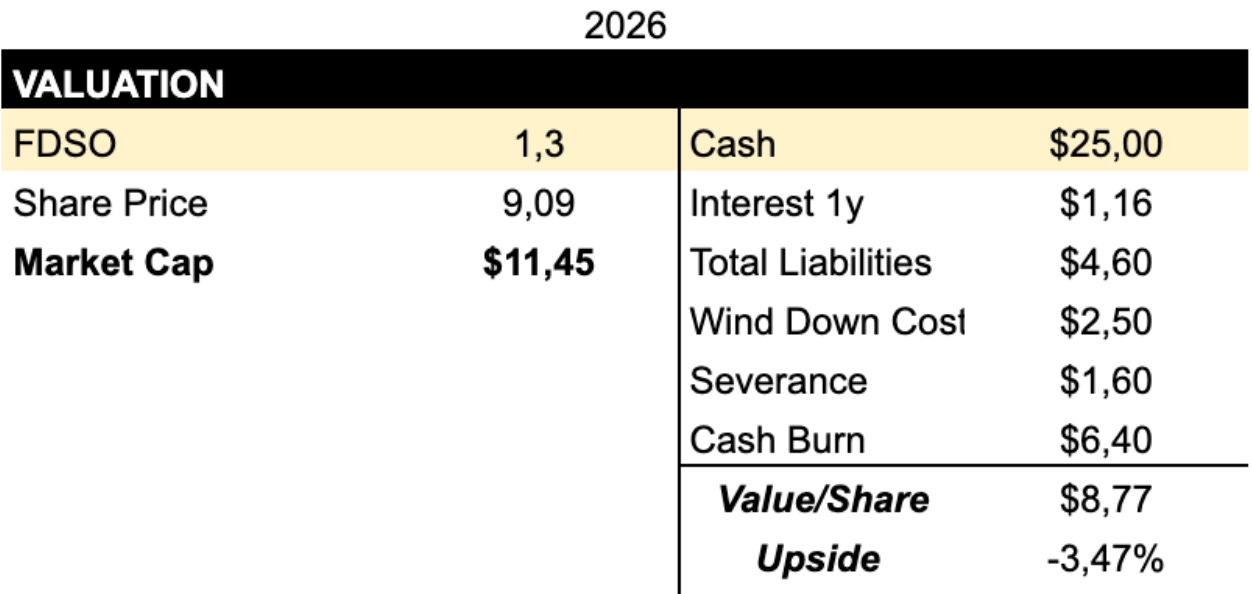

On Feb 17th, I bought shares at $8.86 a pop.

Wait, wait, you said it was worth $8.77/share, and you bought at $8.86 !?

Yap, basically I thought, worst case I don’t lose, but if this plays out as I think it will, all the Biotech hedge funds will buy a very illiquid, nanocap stock at the same time, plus a biotech looking to reverse merge will probably value a premium shell with a lot of cash and no debt at 5-10M USD. (shoutout to Michael Liu again)

Now breath in, breath out…

On Feb 18th, I sold all my shares at $26.357/share. That’s a ≈ 197% return in less than a day. I sold on another account at $31/share, which was closer to 250% return. If we speak about IRR, it approaches infinity…

What Happened?

On February 18, 2026, SNSE announced what was effectively a transformation into Faeth Therapeutics through a reverse-merger-style transaction. In practical terms, it followed a familiar biotech playbook: the public listing remained in place, but control and most of the economic ownership shifted to the private company.

Alongside the merger, the company also announced a $200 million private placement. Sensei agreed to issue Series B non-voting convertible preferred stock in a financing of roughly $200 million. That piece was important not only because it funded the combined business, but because it made clear that investors were backing Faeth’s pipeline rather than Sensei’s now-discontinued oncology program.

The ownership split highlighted just how complete the transition was. Immediately after the merger, former Sensei shareholders were expected to own about 10.7% of the company on a fully diluted basis, while former Faeth shareholders would own roughly 89.3%. After the concurrent financing, legacy Sensei holders were expected to be diluted further, down to about 4.9%, with Faeth holders at 40.8% and the new investors owning 54.3%.

As Michael and I expected, biotech-focused funds wanted in on the drug, and hence the stock, from day one. That demand helped push the value of SNSE’s position to a meaningful premium.

Lessons Learned

Extreme outcomes are extremely shapped by luck, Feb 17th was a public holiday in Portugal, if I wasn’t home to spend the whole day doing research on SNSE, and hadn’t pulled the trigger that same day I would have missed it, not to speak of the fact that if Michael didn’t share the idea with me I wouldn’t even know this case existed or these setup was a thing.

It’s worth going the extra mile. I only invested because I did some forensic research on the new board member who, as I discovered, happened to have a history of reverse mergers and, I suspected, had his bonus tied to a corporate transaction.

These things shouldn’t happen, and yet they do… I think more than the money I made on the trade, I re-learned a value lesson: be humble, and hustle. If you’re a young guy with a very small capital base, you are able to get into these extremely quirky situations and expose yourself to extreme outcomes like this one without much risk. I think of this as the equivalent of the lemonade stand or lawn mowing in investing, you can only do it when you’re young, ambitious, and aren’t afraid to experiment, you never know when someone (the market) will tip you with $100.

Now, the pitch that goes along with this case study is behind a paywall for a couple of reasons

It’s an extremely illiquid company, and I am fully aware of the effects that one Substack post can have on a stock

I still want to document my thought process publicly.

I have 5 loyal paid subscribers who are basically doing charity since they could get the same info for free, so I’m aiming to give something back to them.

Once I sell the stock, I’ll remove the paywall.

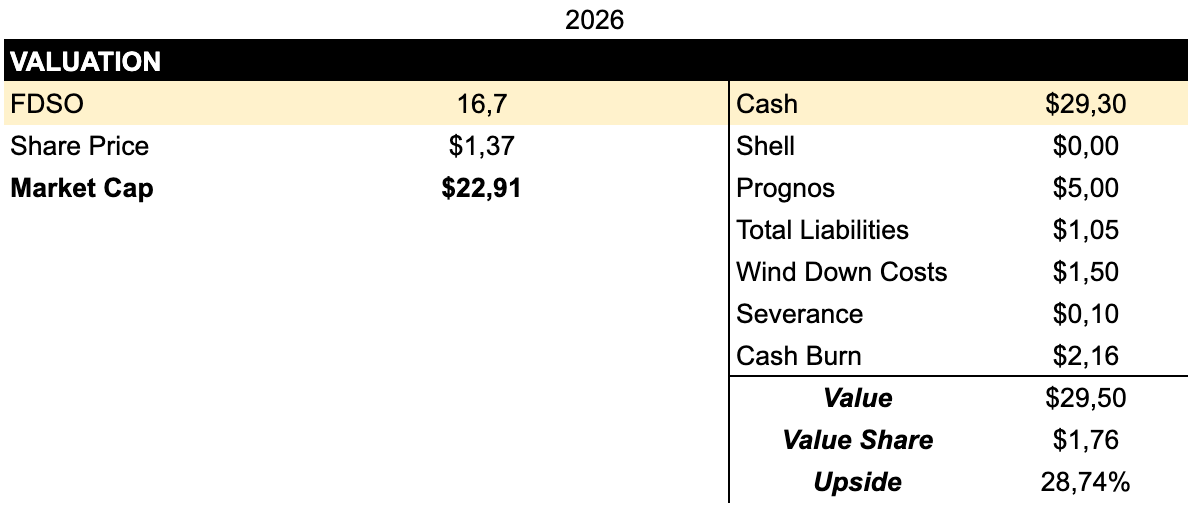

UPDATE I SOLD SFES: at $1.51 USD as the discount to cash got thinner, and hence the IRR didn’t look so attractive.

The Pitch: $SFES - Safeguard Scientifics Inc

This is an OTC Pink Listed Stock, and therefore, I could only buy it for 3/5 accounts I manage due to some restrictions. In any case, my average price on the shares was around $0.7147 USD.

Description

To understand Safeguard Scientifics’ current valuation and the scale of the dislocation around it, it helps to look at how the company has evolved over the past decade. Safeguard was once a well-regarded publicly traded venture capital firm, investing in early- and growth-stage businesses across healthcare, digital media, and financial services. Its model was straightforward: take minority stakes in promising private companies, often with board representation, and help guide them toward an acquisition or IPO.

Over time, though, that structure became harder to sustain. Weak conditions in the micro-cap public markets, combined with the rising cost of being a public company and meeting SEC reporting requirements, put increasing pressure on the model. Maintaining a listed holding company around a smaller portfolio of private investments no longer made economic sense.

That led to a decisive shift in January 2018. Safeguard stopped making new investments and instead focused entirely on supporting and monetizing its existing portfolio. The goal became clear: maximize realizations and return capital to shareholders. In effect, the company moved away from operating as an active venture investor and began functioning more like a vehicle in orderly runoff, with management’s priorities centered on asset sales and capital returns.

Recent Exits

Exit 1: meQuilibrium (August 2025)

The first of the three exits included in the company’s trailing twelve-month total, as referenced in the March 2026 announcement, was meQuilibrium. Based in Boston, meQuilibrium provides digital coaching and engagement tools that use behavioral psychology and data science to deliver personalized resilience programs for employers and health plans. Safeguard had long held a meaningful ownership stake, generally in the range of 30.1% to 33.1%.

In August 2025, meQuilibrium completed a merger with Magnum Merger Sub, Inc., a wholly owned subsidiary of RippleWorx, Inc. As part of that transaction, Safeguard received $1.96 million in cash for its full 30.1% stake, fully exiting the investment. Because the deal closed in the third quarter of 2025, those proceeds were already reflected in the company’s $9.119 million cash balance as of September 30, 2025. Still, since the sale fell within the trailing twelve-month period ending in March 2026, it represented the first piece of the $23.5 million aggregate figure cited by management.

Exit 2: Aktana (January 2026)

The second major liquidity event involved Aktana, a company focused on AI-driven decision support and omnichannel marketing optimization for life sciences sales teams. Headquartered in San Francisco, Aktana built its business around a proprietary Contextual Intelligence Engine that uses machine learning to help pharmaceutical sales and marketing teams improve how they engage with prescribing physicians. Safeguard identified the opportunity early, leading Aktana’s Series B financing in June 2016 and retaining a minority stake that ranged from roughly 13.6% to 18.9% over time.

On January 7, 2026, it was announced that PharmaForceIQ, backed by private equity firm Eir Partners, had acquired Aktana. Strategically, the deal combined Aktana’s AI-based “Next-Best-Action” technology with PharmaForceIQ’s digital orchestration platform, creating a broader solution for the pharmaceutical industry. Because the transaction closed in the first quarter of 2026, the cash proceeds attributable to Safeguard’s stake were not reflected in the third-quarter 2025 balance sheet and therefore represented new cash inflows.

Exit 3: Moxe Health (March 2026)

The final exit in the sequence was Moxe Health. Founded in 2012 and based in Madison, Wisconsin, Moxe operates as an electronic health record integration platform and clinical data clearinghouse. Its main products, Substrate and Convergence, support the two-way exchange of clinical, analytical, and administrative data between healthcare providers and payers, helping streamline workflows tied to risk adjustment, quality monitoring, and prior authorization. Safeguard first invested in Moxe in September 2016, leading a $5.5 million Series A round, and ultimately built a 19.2% ownership stake.

On March 13, 2026, Safeguard announced that BV Investment Partners had completed a majority investment in Moxe Health, giving Safeguard a clear exit from another long-held position. Like the Aktana transaction, the proceeds came well after the close of the third quarter of 2025, meaning they were not yet reflected in the earlier reported cash balance.

The corporate announcement explicitly linked an aggregate of $23.5 million in total cash proceeds to the "three investment exits within the last twelve months," definitively identifying Moxe as the third. Given the chronological timeline of events, these three specific exits are mathematically confirmed to be meQuilibrium (August 2025), Aktana (January 2026), and Moxe Health (March 2026).

Valuation

One might think that after a +100% surge in the stock price, the party has ended. Might be true, but let’s look at some facts.

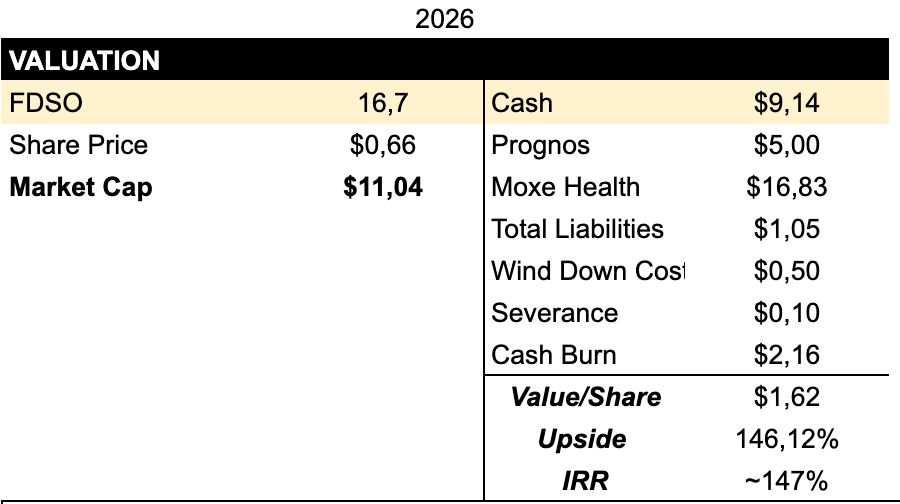

This was the original model I built when I first started buying shares in late February 2026.

Based on the latter outcome, it appears Safeguard was able to monetize Moxe at a valuation close to the one I initially assigned to it.

I adjusted the cash figure by factoring in another month or so of operating cash burn, adding the expected proceeds from Aktana and Moxe, and subtracting the accrued LTIP payout. That gets me to my estimated cash balance.

I assign little to no value to the shell itself.

That leaves Prognos as the only meaningful asset still on the balance sheet, with Safeguard owning ∼19% of the equity. The historical cost basis is $17.6 million, and the position was marked down to just $3 million in mid-2022. Given that SFES invested another $3 million in 2023, I think a more reasonable estimate today is around $5 million.

On that basis, SFES appears to have about $1.64 per share in net cash while the stock is trading at $1.37, implying roughly a 20% discount. On top of that, investors are effectively getting the Prognos stake for free. My view is that the stock should move closer to net cash per share once the company announces a special dividend, and if the liquidation process is completed efficiently, there may be another 8% to 10% of upside.

The main risk is timing. Prognos could take years to monetize, and if that happens, the IRR becomes far less attractive. My plan is to exit before that point, ideally if and when the stock converges toward its net cash per share value.

Thanks for Reading!

Hi David, thanks for the great write up! I saw you mentioned “Safeguard stopped making new investments and instead focused entirely on supporting and monetizing its existing portfolio. The goal became clear: maximize realizations and return capital to shareholders” and was wondering if management is truly committed to a full, timely wind-down or if they might be hoarding excess cash with no clear accelerated return plan to shareholders.